Rent To Own Homes Spokane Watypography

Hey, you! Yeah, you, the one scrolling endlessly, dreaming of your own little slice of Spokane. Ever feel like homeownership is this super exclusive club, with velvet ropes and bouncers named "Mortgage Broker" keeping you out? I hear ya! It's like, "Gotta have a down payment the size of a small country, and a credit score higher than Mount Spokane." Phew. Exhausting, right?

But what if I told you there's a way to maybe, just maybe, get your foot in the door, no velvet rope in sight? We're talking about rent-to-own homes in Spokane. Ever heard of that? It's kinda like this cool shortcut, a little wink-wink nudge-nudge deal that could get you into a place you actually love. Think about it – no immediate insane down payment! Score!

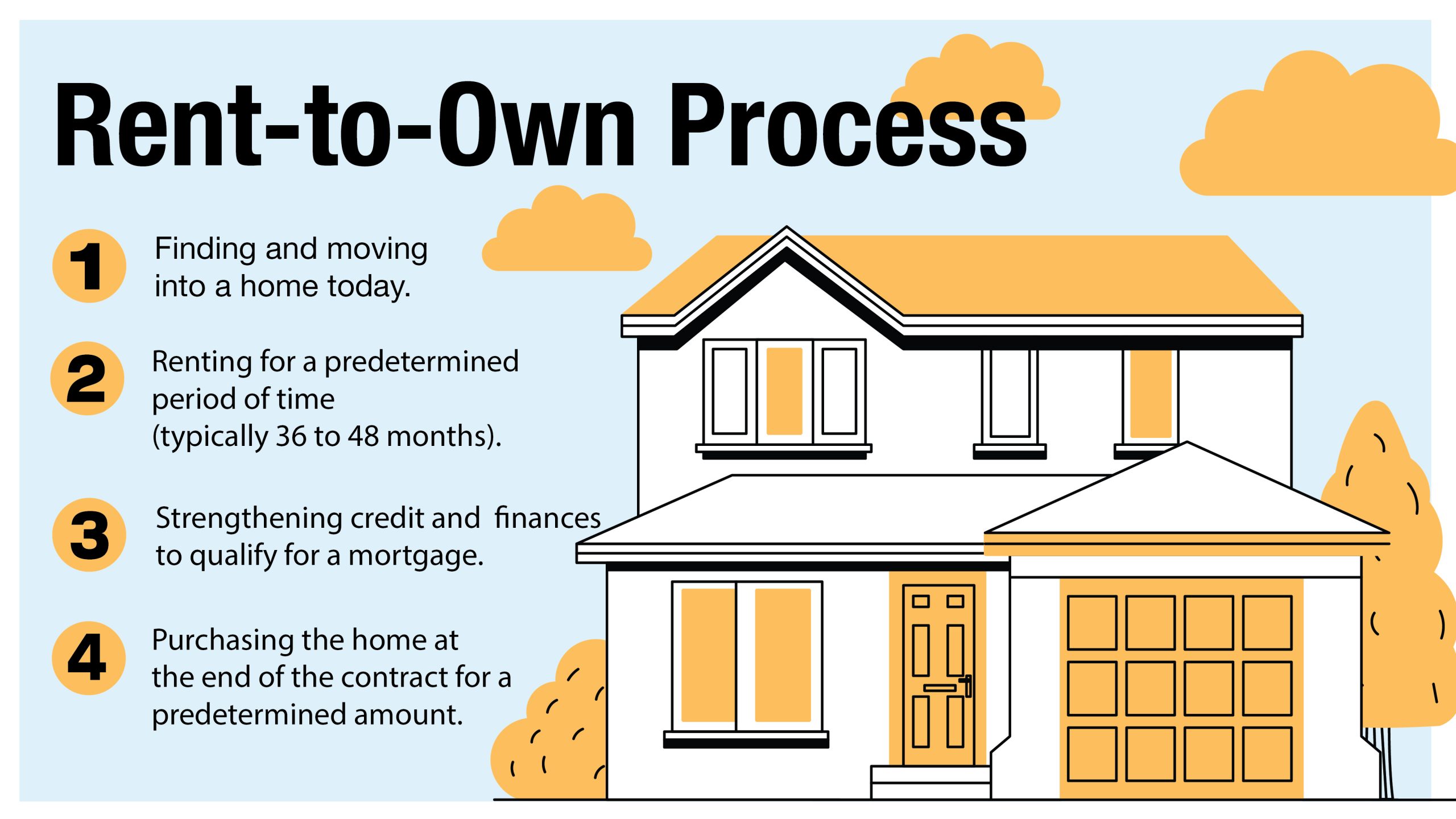

So, what is this magical creature, this rent-to-own home? Imagine this: you find a house in Spokane that just speaks to you. It’s got that perfect little yard for barbecues, a kitchen where you can actually whip up your famous chili, and maybe even a room that’s begging to be your epic gaming den. You don't have to buy it today, today. Nope. Instead, you sign an agreement with the owner. You get to live in it now. How sweet is that?

Must Read

- A Quiet Escape In The Suburbs: Visiting Union Pond Conservation Area

- Conquer Manitoulin’s Best View: Cup And Saucer Trail Parking & Trailhead Guide

- 140 Kilometers Of Adventure: Biking The Greater Niagara Circle Route

- Scenic Routes For Every Fitness Level: The Best Walking Trails Niagara Falls Offers

- Eksplorasi The Highest Point Of The Escarpment: Pretty River Provincial Park

And here's the kicker: part of your monthly rent? It actually goes towards the purchase price of the house. It's like your rent is giving you a high-five and saying, "You're on your way to owning this!" Pretty neat, huh? It’s like a little savings plan built right into your living situation. Who knew paying rent could feel so… productive?

Now, before you start mentally redecorating your new Spokane abode, let’s pump the brakes for a sec. This isn't a magic wand, folks. It’s a contract. And contracts, my friends, are serious business. You gotta read every single word, like you're a detective solving the case of the missing sock. What are the terms? What’s the purchase price? What happens if you miss a payment? These are the juicy details you need to know.

Think of the agreement as your roadmap to homeownership. You want that roadmap to be crystal clear, with no hidden detours or surprise potholes. So, when we’re talking about rent-to-own in Spokane, we’re talking about doing your homework. No skimping! Get it? Homework. Even though you’re already living there. The irony is not lost on me.

One of the biggest perks, obviously, is the whole “less money upfront” thing. Let’s be honest, saving for a down payment can feel like climbing Everest in flip-flops. It’s daunting. It’s demoralizing. It makes you want to just live in a really nice tent. Rent-to-own lets you skip that initial mountain climb, or at least start on a gentler slope. You get to live in your potential future home while you save up the rest.

And this isn't just for folks who are, like, totally new to the housing market. Sometimes, life throws curveballs. Maybe your credit took a little hit, or your income isn't quite where you want it to be right now. Rent-to-own can be a fantastic bridge for those situations. It gives you time to get your financial ducks in a row, while still enjoying the stability of a home.

Plus, Spokane itself! It’s not just some generic city, right? It's got that vibrant downtown, those amazing hiking trails, that whole Riverfront Park vibe. Finding a rent-to-own place here means you can start soaking up all that Spokane goodness now, not after you’ve finally conquered your down payment dragon. You can be part of the community, exploring local breweries and finding your favorite coffee shop before you even officially own the roof over your head.

So, what kind of rent-to-own agreements are we talking about? There are a couple of flavors, like choosing between a latte and a cappuccino. One is called a "lease-purchase agreement." This is where you agree to buy the home at a specific price at the end of your lease term. Simple enough, right? It's a straight-up commitment to buy, just with a delayed closing date.

Then there's the "lease-option agreement." This one's a bit more flexible. You have the option to buy the home at a predetermined price. It's like having a reservation at your dream restaurant. You've got dibs, but you're not obligated to eat there if you change your mind. This can be great if you're still a little unsure or need more time to solidify your finances.

Now, let’s talk about the nitty-gritty, the stuff that makes your eyes glaze over but is super important. The "option fee." This is usually a one-time, non-refundable payment you make when you sign the lease-option agreement. It’s like a down payment on your option to buy. Think of it as paying for the right to consider owning the home.

And that rent credit we mentioned? This is usually a portion of your monthly rent that gets applied towards the purchase price. It’s a sweet bonus! So, you’re paying for shelter, and you’re also building equity. It’s like getting paid to live in your future home. Almost. Not quite, but close enough to feel good!

The purchase price is obviously a huge deal. You and the seller will agree on this upfront. This protects you from a sudden market surge that could skyrocket the price by the time your lease is up. You’ve locked in your price, like a seasoned negotiator who’s just secured the best deal in town.

The lease term is also critical. This is the length of time you’ll be renting the home before you’re expected to buy it. It could be a year, two years, maybe even longer. This gives you a clear timeline for your homeownership journey. So, you know when you need to be ready to sign on the dotted line.

What about closing costs? These are the fees associated with finalizing the sale of a home. They can include things like appraisal fees, title insurance, and loan origination fees. You need to understand who is responsible for these costs in your rent-to-own agreement. Is it you? Is it the seller? Is it a shared pot of gold? Find out!

And the home inspection! Oh, the home inspection. This is like a doctor's visit for your potential new house. You absolutely must get a professional inspection. You don't want to buy a house that’s secretly harboring a family of raccoons in the attic or a leaky roof that’s developing its own ecosystem. A good inspector will tell you if the house is healthy, or if it needs some serious TLC.

This is especially important with rent-to-own because you might be buying the house "as-is" or with fewer warranties than a traditional sale. So, that inspection report is your best friend. Treat it like gold. Because it is!

Now, let’s talk about what happens if things don't go according to plan. Life happens, right? Maybe you lose your job, or you have an unexpected medical emergency. What happens to your option fee? What happens to the rent credits you’ve accumulated? Your contract should clearly outline this. You need to know your exit strategy, so to speak.

Sometimes, if you can't fulfill the contract, you might forfeit your option fee and any rent credits. Ouch. That’s why it’s so important to be realistic about your financial situation and your ability to stick to the agreement. Don't go into it with rose-tinted glasses if your bank account is currently wearing a pair of tattered sweatpants.

It’s also a good idea to have a backup plan for securing financing. Even though you're in a rent-to-own situation, you'll eventually need a mortgage to finalize the purchase. Start talking to lenders early, understand your credit score, and see what you qualify for. This will give you a realistic picture of your financial future.

And get this – sometimes, you might even have the opportunity to negotiate the purchase price again at the end of the lease term, especially if the market has changed significantly. It’s not always set in stone, but that depends entirely on your specific agreement. So, read that contract like you’re deciphering ancient hieroglyphics, because those little clauses can make a big difference!

When you're looking for rent-to-own homes in Spokane, where do you even start? Well, a good place to begin is by looking for real estate agents who specialize in these types of transactions. They'll have a better understanding of the local market and can help you find listings. You can also search online. There are websites dedicated to rent-to-own properties.

And don't be afraid to talk to people! Ask friends, family, or colleagues if they've ever used a rent-to-own program. You never know who might have some insider tips or know of a great opportunity in Spokane.

The key takeaway here is that rent-to-own is a viable option for many people looking to own a home in Spokane. It’s not a get-rich-quick scheme, and it's definitely not a way to avoid all financial responsibility. But it is a way to make homeownership more accessible, more manageable, and maybe even a little bit more fun. It’s a stepping stone, a bridge, a pathway to having your own place that you can truly call yours.

So, if you're tired of renting and dreaming of putting down roots in Spokane, start exploring the rent-to-own world. Do your research. Ask questions. Read everything. And who knows? You might just find yourself signing the papers on your dream Spokane home sooner than you think. Wouldn't that be something?

Imagine hosting your first Thanksgiving dinner in your own kitchen. Or planting those ridiculously cheerful petunias in your own garden. Or just lounging on your own couch without worrying about your landlord coming over for an impromptu inspection. That's the dream, right? And with rent-to-own, that dream might be closer than you think. Go get 'em, Spokane home seeker!

![Are Rent To Own Homes A Good Idea? [Here's How It Works]](https://investedwallet.com/wp-content/uploads/2020/08/rent-to-own.jpg)