Homeowners Insurance Policy Quote: How Rising Construction Costs Impact 2026 Rates

Hey there, fellow homeowners! So, you're probably thinking about that homeowners insurance policy quote, right? Maybe you just got one, or maybe you’re bracing yourself for what’s coming. Let’s be honest, talking insurance can feel about as exciting as watching paint dry, but stick with me here, because we’re going to dive into something that’s directly affecting those numbers: rising construction costs, and how that’s likely to throw a wrench into our 2026 rates. Think of me as your friendly neighborhood insurance decoder, minus the stuffy jargon and the urge to offer you a lukewarm cup of decaf.

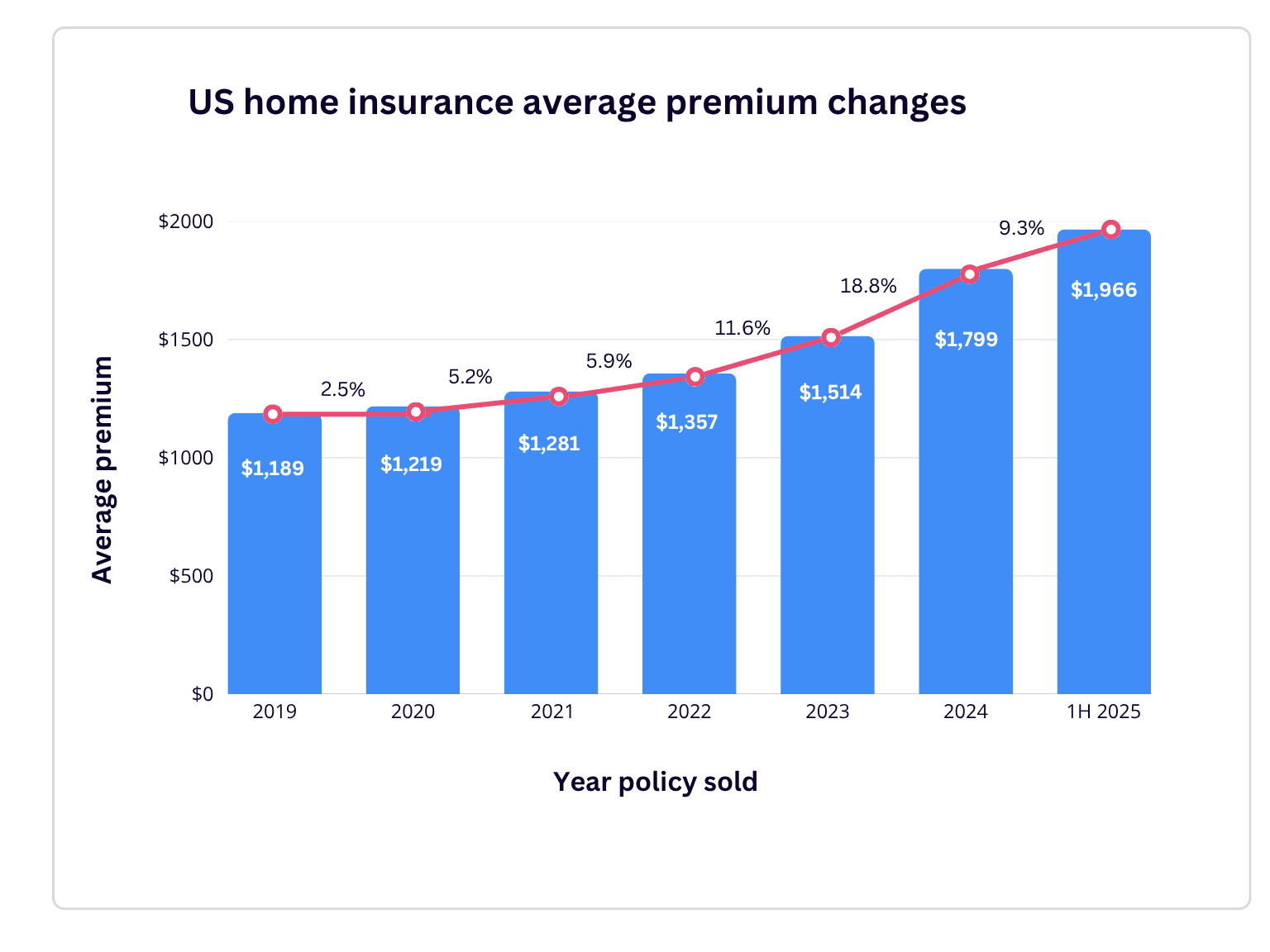

First off, why are we even talking about 2026? Well, insurance policies are typically renewed annually, so whatever happens this year, next year, and the year after that, will eventually trickle down to your renewal premium. And right now, there's a whole lot happening in the world of building things that's making everything more… well, expensive.

The Great Stuffing of the Supply Chain Pockets

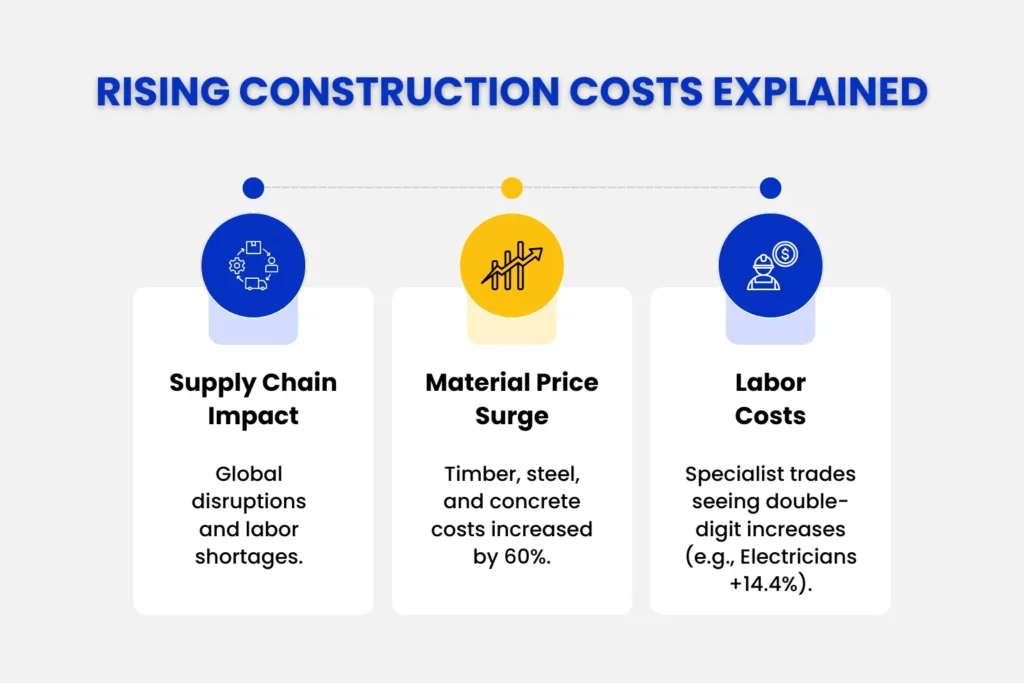

Remember when we were all a little stressed about toilet paper shortages? That was just the tip of the iceberg, folks. The global supply chain has been a bit of a rollercoaster, and while some things are easing up, others are still feeling the pinch. Think about it: all those lovely materials that go into building or repairing your home – lumber, steel, concrete, even those fancy shingles you’ve been eyeing – they all have to be produced, shipped, and delivered. And when any part of that journey gets bumpy, prices tend to go up. It’s like trying to get your favorite artisanal sourdough delivered from across the country; there are a lot of variables!

Must Read

- A Quiet Escape In The Suburbs: Visiting Union Pond Conservation Area

- Conquer Manitoulin’s Best View: Cup And Saucer Trail Parking & Trailhead Guide

- 140 Kilometers Of Adventure: Biking The Greater Niagara Circle Route

- Scenic Routes For Every Fitness Level: The Best Walking Trails Niagara Falls Offers

- Eksplorasi The Highest Point Of The Escarpment: Pretty River Provincial Park

This isn’t just a minor hiccup. We’re talking about significant price increases for the raw ingredients of our homes. And guess who ends up footing the bill? Yep, you and me, when it comes time to rebuild or repair.

Labor Pains: The Not-So-Glamorous Side of Construction

It’s not just the wood and nails, either. The construction industry, like many others, is facing a shortage of skilled labor. Finding good, reliable contractors, electricians, plumbers – the whole gang – is becoming increasingly difficult. And when demand outstrips supply, what happens? You guessed it: wages go up. This means that the cost of hiring someone to fix your leaky faucet or, heavens forbid, rebuild your entire roof after a storm, is going to be higher.

Imagine trying to book a popular concert ticket on the day of release; everyone wants one, and the prices reflect that scarcity. It’s a similar dynamic in the construction world, just with more hard hats and less screaming.

The Rebuilding Reality: What Happens When Disaster Strikes

This is where homeowners insurance really earns its stripes, right? When the unexpected happens – a fire, a major storm, a rogue squirrel infestation that somehow causes structural damage (hey, it could happen!) – your insurance is supposed to cover the cost of repairs or rebuilding. But here’s the kicker: if the cost to rebuild your home today is significantly more than it was a year or two ago, your existing insurance policy might not be enough.

This is why your insurance company is constantly reassessing the "reconstruction cost" of your home. They're not just looking at the pretty paint color or the number of bedrooms; they're estimating what it would cost to literally build your house from the ground up, using current material and labor prices. And those prices, as we've established, are on the rise.

The 2026 Crystal Ball: What It's Telling Us About Your Premiums

So, how does all this translate to your 2026 homeowners insurance premium? Think of your premium as a kind of financial pot. Your insurance company puts money into that pot from all their policyholders. Then, when someone has a claim, they use money from the pot to pay for it. If the cost of fixing those claims is going up, then the amount of money going into the pot – your premium – generally needs to go up too, to keep the pot from running dry.

Insurance companies are in the business of managing risk. They look at trends, historical data, and current economic conditions to predict how much they'll likely have to pay out in claims. Right now, those predictions are being heavily influenced by the escalating costs of materials and labor. So, even if your home hasn't changed one bit, and you've been the most responsible homeowner since the dawn of time (kudos to you!), you might still see an increase in your premium.

It's Not All Doom and Gloom (Promise!)

Okay, I know this might sound a bit like a financial downer, but before you start weeping into your mortgage statements, let's put on our optimism hats. The good news is that insurance companies are generally pretty good at forecasting. They’re not just waking up one day and deciding to hike prices for fun. These adjustments are usually calculated and phased in to reflect the changing economic landscape.

Plus, understanding these trends empowers you. Knowing that construction costs are a significant factor gives you leverage when it's time to shop around for your next policy. You can ask more informed questions, understand the quotes you receive, and perhaps even explore ways to mitigate the impact.

Proactive Ponderings: What YOU Can Do

So, what can a savvy homeowner like yourself do in the face of these rising rates? A few things come to mind:

- Stay Informed: Keep an eye on news related to the construction industry and inflation. The more you know, the better prepared you'll be. Think of it as doing your homework, but with much less homework to actually do!

- Review Your Policy Annually: Don't just auto-renew. Take the time to go through your current policy. Are your dwelling coverage limits still adequate? Have you made any renovations or upgrades that might increase your home's value (and therefore, its reconstruction cost)? This is your moment to be a policy detective!

- Shop Around: This is the golden rule of insurance. Don't get locked into one provider. Get quotes from multiple insurance companies. Even a small difference in premium can add up over time. It’s like comparing prices at different grocery stores for your favorite brand of ice cream – you want the best deal for your buck.

- Ask About Discounts: Seriously, who doesn't love a discount? Ask your insurance agent about any potential discounts you might be eligible for. Things like having a security system, being claims-free, or bundling your home and auto insurance can make a real difference. It’s like finding that hidden coupon you forgot about!

- Consider Your Deductible: Your deductible is the amount you pay out-of-pocket before your insurance kicks in. Increasing your deductible can lower your premium. However, make sure you can comfortably afford to pay the higher deductible if you ever need to file a claim. It's a trade-off, so weigh your options carefully.

- Understand Replacement Cost vs. Actual Cash Value: This is a big one! Replacement Cost pays to rebuild your home with new materials of like kind and quality. Actual Cash Value (ACV) pays the replacement cost minus depreciation. For most homeowners, replacement cost coverage is the way to go, especially with rising construction costs. Make sure you know what you have!

The "What Ifs" and the "Maybes" of Future Premiums

It's important to remember that these are projections. The construction industry is dynamic, and unforeseen events can always shift the landscape. Perhaps new technologies emerge that dramatically lower material costs, or perhaps a surge in construction workers graduates from trade schools. We can hope for the best, right?

However, for 2026, the trend of rising construction costs is a pretty solid bet. Insurers are already factoring this into their current pricing models, and that will likely continue. The goal is to ensure that when you do need them, they have the resources to help you rebuild your haven.

Looking Ahead with a Smile (Seriously!)

So, while the thought of increasing insurance premiums might feel a bit like finding a gray hair you weren’t expecting, it’s really just a reflection of the world we live in. Homes are valuable assets, and protecting them is paramount. The rising cost of building them means that the cost of insuring them will likely adjust accordingly.

But here’s the uplifting part: you are in control of how you approach this. By being informed, proactive, and a smart shopper, you can navigate these changes with confidence. Think of it as an opportunity to get smarter about your insurance, to ensure you have the right coverage at the best possible price. Your home is your sanctuary, your happy place, and making sure it’s protected is a fundamental act of self-care.

So, take a deep breath, maybe grab a cookie (you've earned it after reading all this insurance talk!), and remember that with a little bit of savvy and a positive outlook, you can absolutely manage your homeowners insurance needs, even in a world of rising building costs. Here's to a well-protected and wonderfully worry-free home in 2026 and beyond!